Iran Walks, June Closes In

Iran halts US ceasefire talks and pledges to “completely” close the Strait, WTI snaps +5.3% in a session, and a stacked BOJ–Fed mid-June window now collides with a softer 30Y auction, a record private

Gatherthink Signals — Risk & Markets Weekly

Issue 4 · 2026-06-08

Geopolitical risk, macro signals, and market transmission — structured, scored, and scenario-mapped.

Bottom Line: Last cycle the Iran trade was bull-leaning on a tentative MOU. This cycle the deal is dead — Iran halted talks and pledged Hormuz closure on or before June 1, and the energy channel reversed in a single session. The bear case at RK-006 returns to 0.45 and composite snaps 80→100. Meanwhile June stacks three catalysts in one week: CPI June 10, the 30Y reopen, and a Fed/BOJ rate decision pair 24 hours apart. The shock absorbers are thinner than they were six days ago.

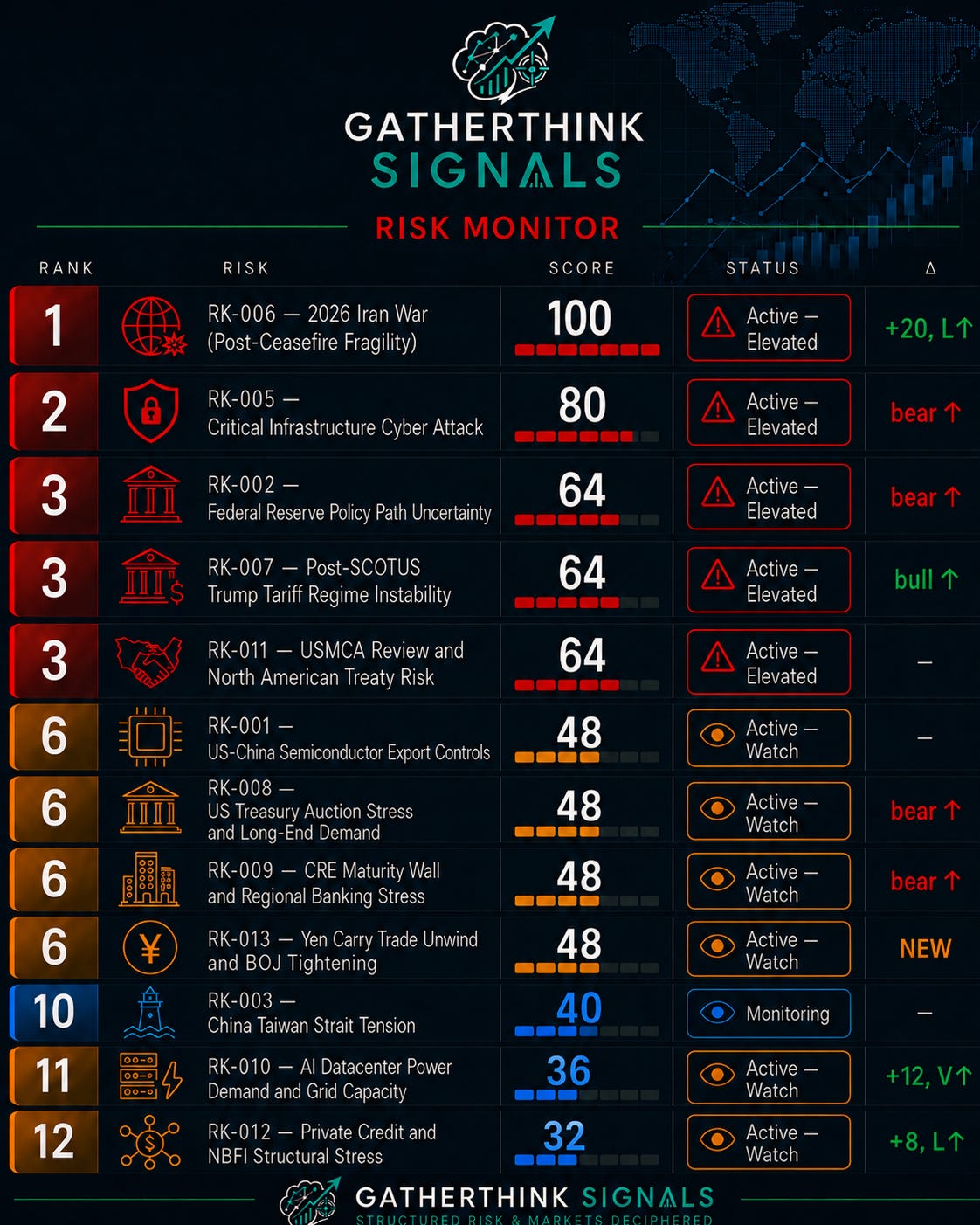

1. Risk Scorecard

Register change: RK-013 added from horizon-scan as the cross-asset macro counterpart to a stacked mid-June calendar. RK-004 remains dormant. RK-010 reactivated last cycle after a residential-bill spillover.

Two composite moves and several scenario shifts. RK-006 jumps 80→100 (likelihood 4→5; bear 0.25→0.45; bull 0.28→0.10) — the Iran MOU is dead, Hormuz pressure is real, WTI is no longer the disconfirming buffer it was a week ago. RK-012 raised 24→32 (likelihood 3→4) on Fitch’s record 6.0% private-credit default print and concentrated BDC stress signals. RK-002, RK-005, RK-008, RK-009 bear probabilities up: each absorbs spillover from a still-tight HY OAS (2.75%) that is not yet pricing what the underlying signals contain.

2. This Week’s Story

Six days ago Iran was a bull-leaning trade. A tentative MOU framework had pulled WTI from $112 to $97, and the brief’s deep dive moved on to the USMCA. The MOU was always unsigned — markets priced the probability, not the signature — but the framework was alive, the backchannels were open, and Fed math had been re-anchored on energy disinflation.

The framework died. Iran halted backchannel communications with the US on or before June 1 and pledged publicly to “completely” block the Strait of Hormuz, citing continuing ceasefire violations including Israeli operations against Hezbollah. The energy channel reversed in one session — WTI $91.16 on May 29 to $95.96 on June 1, +5.3% in a single print (FRED). Trump never signed. The Bull–Bear walk-back from the prior issue has gone the other direction.

The mechanical consequence is that a single risk now sits at composite 100 — the top of the Elevated band — with bear probability at 0.45 and the full transmission stack reactivated: oil, safe-haven flow, credit, geopolitical premium, cyber retaliation. The same energy reversal that drives RK-006 also raises the bear cases on RK-002 (Fed cannot dovishly absorb an oil-fed CPI), RK-005 (Iranian cyber motive restored), and RK-008 (oil-inflation premium intersects a softer long-end auction backdrop).

And the calendar tightens. June 10 CPI, June 15 30Y reopen, June 16–17 FOMC with SEP and dot plot, June 16–17 BOJ — four catalysts inside one week, with the Iran shock as backdrop. The week’s story is not a single event. It is the stack.

3. Top Risk + Deep Dive: RK-006 — 2026 Iran War (Score: 100 | Elevated)

What happened. Iran halted backchannel ceasefire communications with the United States on or before June 1, 2026 and publicly pledged to “completely” block the Strait of Hormuz, citing continuing ceasefire violations including Israeli operations against Hezbollah. The tentative MOU framework that anchored Cycle 7 and 8’s de-escalation thesis is now functionally broken. Trump never signed. Iran and allies pledged to activate additional fronts, including Bab al-Mandeb. Hormuz ship traffic, already below pre-war baselines since April 8, no longer has an upper bound on disruption. FRED confirms the energy reaction: WTI $91.16 on May 29 → $95.96 on June 1, a single-session 5.3% jump.

Bull (p=0.10), base (p=0.45), bear (p=0.45). The bull case requires diplomatic re-engagement within weeks, partial Hormuz disruption that is walked back, WTI returning to $85–92 by Q3, and a fast-fading safe-haven premium — none of which is visible today. The base case holds Iran’s rhetorical blockade as partly bluff: effective throughput falls further but the Strait does not close fully, WTI holds $93–105 with episodic spikes, the Fed delays cuts, energy inflation passes through to summer CPI, the ceasefire remains technically intact but unenforceable. The bear case is material Hormuz closure (mines, naval action, or tanker attacks), WTI above $115, HY OAS widening from 2.75% toward 4%, Iranian cyber retaliation hitting US critical infrastructure (the live RK-005 channel), and the Fed forced into a hawkish hold.

Market transmission. Five channels are now all active simultaneously: commodity-price (WTI is the daily pricing mechanism), safe-haven flow (GLD, TLT, USD), credit-tightening (HY OAS at 2.75% is the canary — 3.5% is warning, 4.0% is bear confirmation), geopolitical premium (selective dollar bid, regional asset stress), and supply-disruption (refining flows, LNG, Asian crude routing). XLE, OIH, and GLD are the most direct beneficiary trades in the bear case; TLT and EEM are the most exposed downside trades; UUP behavior remains the disconfirming evidence on whether this is selective or systemic risk-off. Market confirmation (macro): WTI +5.3% single-session on Iran shock (FRED DCOILWTICO $91.16 → $95.96, May 29 → Jun 1) confirms the commodity-price channel; HY OAS 2.74% (FRED Jun 4) shows no parallel public-credit signal; DGS10 stable at 4.49% (FRED Jun 3); broad dollar weakening (DTWEXBGS 118.88, May 29) does not yet support a selective dollar bid. Equity/ETF snapshot not captured this cycle.

Bear trigger to watch. A confirmed Hormuz physical disruption event — a mine detonation, naval action, or tanker attack — is the single move that takes composite from 100 to the Critical band (101–125). HY OAS crossing 3.5% would be the public-credit confirmation. Iranian cyber attribution on US critical infrastructure (cross-link RK-005) is the third trigger and the one that broadens the channel set.

5. The Others

RK-005 — Critical Infrastructure Cyber Attack (Score: 80, bear ↑): CISA advisory gap now 59 days — the planned 60-day downgrade is off the table because the Iran restraint thesis that anchored it has decayed. Itron breach (April 27) confirms vendor-side supply-chain exposure across thousands of utilities; Iranian state-sponsored targeting of US water utilities documented across multiple sources.

RK-002 — Federal Reserve (Score: 64, bear ↑): June 16–17 FOMC SEP meeting. CME implies ~65% hold / ~33% 25bp cut; iShares puts cut probability at 14%. Iran oil shock complicates a dovish path; bear raised to 0.35 on the parallel BOJ catalyst and a softer long-end backdrop.

RK-007 — Tariff Regime (Score: 64, bull ↑): CIT 2-1 injunction blocked Section 122 fallback tariffs on May 7. CBP CAPE processed $85B in refund applications; $20.6B sent to Treasury. Two legal authorities (IEEPA + Section 122) are now gone — bull raised to 0.20, base reduced to 0.50.

RK-011 — USMCA (Score: 64, —): July 1 review opens with Canada formally requesting a 16-year renewal (June 1). Round 2 June 16–17 in Washington. CIT Section 122 block weakens US tariff leverage entering the review; treaty bear case is unchanged but the negotiation posture is materially different than seven days ago.

RK-001 — US-China Semiconductors (Score: 48, —): MATCH Act status quo. Senate S.4281 at introduction stage, House H.R.8170 cleared committee April 22, no floor vote scheduled in either chamber. Score drift flagged at four cycles unchanged.

RK-008 — Treasury Auction Stress (Score: 48, bear ↑): May 13 30Y auction cleared C grade — 5.046% high yield, 5.6bp tail, 2.30 bid-to-cover. Japan sold ~$30B USTs in Q1 (fastest pace in four years). Bear up to 0.30 on BOJ parallel catalyst and oil-inflation premium.

RK-009 — CRE / Regional Banks (Score: 48, bear ↑): Half of Q1 office buildings sold traded at “distressed pricing”; LA at 50-60% discounts; Chicago Loop at $14/sqft. Aggregate NCO modest at 0.63% but PDNA in CRE/multifamily remains elevated. $2T maturity wall ahead.

RK-013 — Yen Carry / BOJ (Score: 48, NEW): BOJ at 0.75% (30-year high); three members publicly called for further hikes (April 28). June BOJ meeting expected to deliver 1.0%. JGB 10Y at ~2.8% (25-year high). Direct cross-link to RK-008 long-end demand and RK-002 Fed simultaneity.

RK-003 — Taiwan Strait (Score: 40, —): No 1H 2026 PLA exercise announced. By post-Pelosi pattern, a 1H exercise is now statistically overdue. The absence is the signal; monitoring continues.

RK-010 — AI Datacenter Power (Score: 36, +12): PJM 2026-27 capacity cleared $329.17/MW — 10x prior year. Data centers = 40% of December auction cost; residential bill impact ~+15%. Velocity 2→3 because the household-bill spillover converts industrial-policy into political risk.

RK-012 — Private Credit / NBFI (Score: 32, +8 / L↑): Fitch private credit default rate hit a record 6.0% TTM through April (up from 5.7% March). BlackRock TCP NAV marked down 19%. Blue Owl tech BDC withdrawal requests 40.7%. HY OAS at 2.75% — no parallel public-credit signal. Channel divergence is the central tension.

6. What Could Be Wrong

The dominant risk to this issue’s framing is that Iran’s “complete blockade” pledge is Persian-Gulf bluff. Full closure is operationally costly to Iran given its own oil revenue dependence and China’s structural opposition (40% of Chinese oil flows through Hormuz). HY OAS at 2.75% — wider but still historically tight — and a weakening USD broad index in late May together argue markets do not yet read this as systemic. Trump retains diplomatic optionality on a days-not-weeks timeline; the backchannel halt is bilateral, not multilateral. Gulf Arab states have economic incentives to mediate. If any of those dampers fire, RK-006’s likelihood retreats and the bear case collapses faster than it rose.

7. What to Watch

WTI daily price and Hormuz physical events (RK-006): A confirmed physical disruption (mine detonation, naval action, tanker attack) is the single move that takes RK-006 from Elevated to Critical. WTI above $108 within days is the price-side confirmation; HY OAS crossing 3.5% is the credit-side confirmation.

May CPI — June 10 (RK-002): The decisive pre-FOMC data point. Tariff-sensitive categories already running hot; if Iran shock prevents moderation, June 17 SEP and dot plot land hawkish into a fragile macro stack.

30Y Treasury reopen — week of June 15 (RK-008): Lands between June 10 CPI and June 17 FOMC. A tail above the May 13 5.6bp would confirm demand fragility into the BOJ parallel; 5.5% on DGS30 is the bear escalation threshold.

BOJ June meeting + FOMC June 16–17 (RK-013, RK-002): A 24-hour window of stacked rate decisions. A BOJ 50bp surprise or accelerated forward guidance against a Fed hawkish hold materially raises cross-asset volatility; USD/JPY break of key technical level signals carry unwind.

CISA/FBI advisories on Iranian actors (RK-005): The 60-day gap closes June 6. Any new advisory naming bulk power, financial core utilities, or Itron-class supply-chain compromise triggers an immediate bear rescore.

Disclaimer: Gatherthink Signals is for educational and informational purposes only. It is not investment, legal, tax, or financial advice. It does not consider any individual’s objectives, financial situation, or risk tolerance. Nothing here is a recommendation to buy, sell, or short any security, asset, or derivative. Readers should do their own research and consult qualified professionals before making financial decisions.