Gatherthink Signals — Risk & Markets Weekly

Geopolitical risk, macro signals, and market transmission — structured, scored, and scenario-mapped.

Issue 1 · May 11, 2026

Welcome to issue number one of Gatherthink Signals, a weekly scenario map for AI, markets, geopolitics, technology risk, and macro uncertainty.

Bottom Line: The dominant risk this week isn’t any single event — it’s the sequence. Iran-driven energy inflation hits the April CPI print on Tuesday just as Kevin Warsh takes over the Federal Reserve on Friday with a mandate-narrowing agenda. Between those two events, Trump and Xi meet in Beijing. The key question: does this resolve into disinflation and détente, or higher oil, a stronger dollar, and tighter financial conditions heading into H2?

This Week’s Brief

Six risks tracked. Three catalysts in the next six days. One of the most consequential weeks of 2026 is about to land.

April CPI drops Tuesday (May 12). Kevin Warsh takes over the Federal Reserve on Friday (May 15). Between those two events, Donald Trump and Xi Jinping sit down in Beijing for the first time since the Iran War ended. Each of these events, in isolation, would be a major market catalyst. They are happening in sequence, across five days, against a geopolitical backdrop that hasn’t been this compressed since the 2022 Russia-Ukraine invasion.

Here is what we know, what we think happens next, and what the evidence says we might be getting wrong.

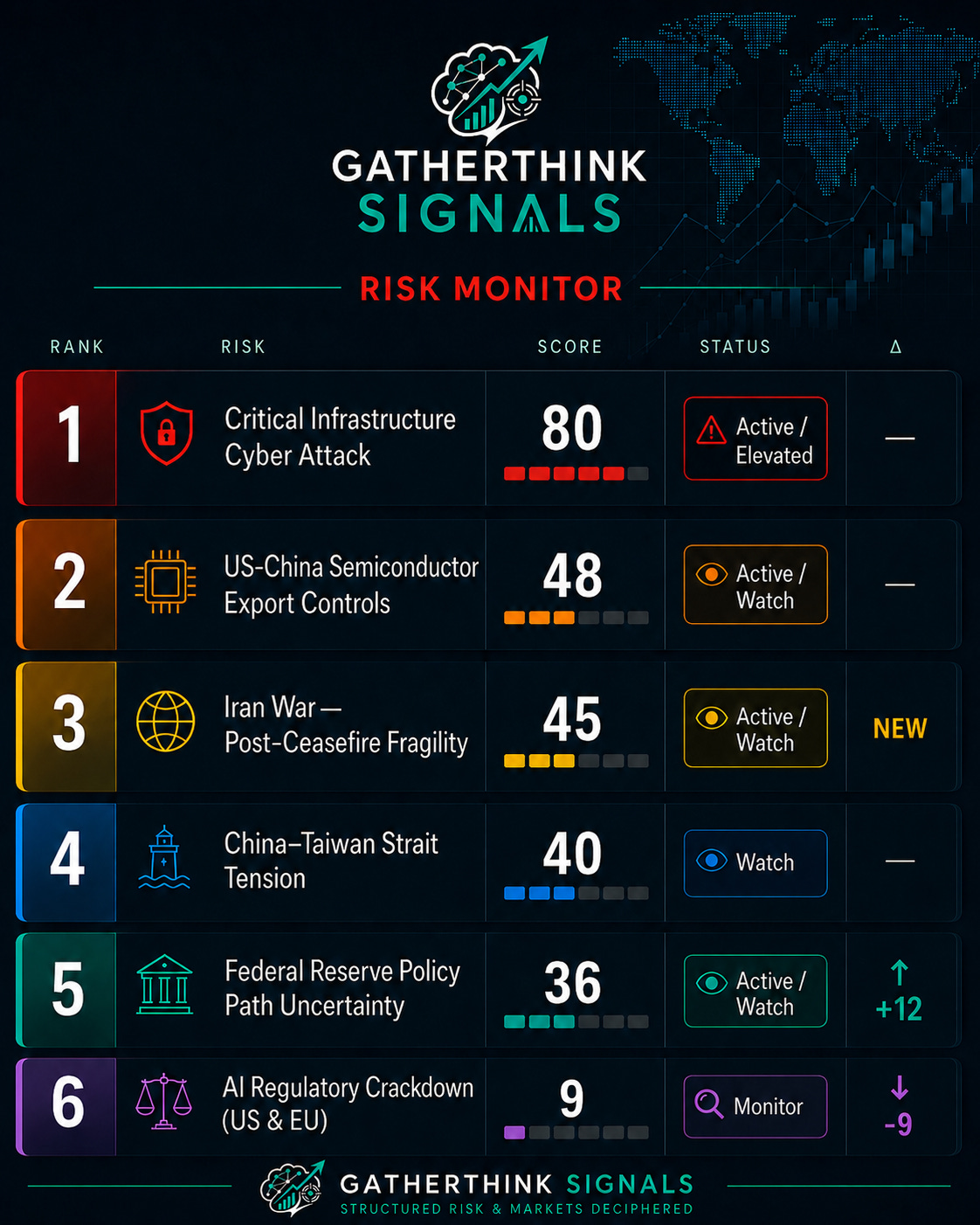

Risk Scorecard

Score = Likelihood × Impact × Velocity (1–125 scale). Thresholds: Monitor ≤20 · Watch 21–60 · Elevated 61–100 · Critical 101–125.

Two risks moved this cycle. RK-002 escalated +12: March CPI came in at 3.3% on the back of a 21.2% gasoline spike — directly Iran-driven — and Kevin Warsh cleared Senate Banking Committee 13-11, the most partisan Fed chair vote in history. Materialization window: days, not weeks. RK-004 fell −9 to Monitor: the EU Digital Omnibus reached provisional agreement on May 7, deferring the August AI compliance deadline to December 2027. RK-006 added: the Iran War post-ceasefire fragility was formalized as a standalone risk — it has been shaping every other risk for months and now has its own score.

This Week’s Story

The 2026 Iran War officially ended April 7–8. What it left behind has not.

The Strait of Hormuz remains at approximately 5% of pre-war vessel traffic. WTI averaged $91 per barrel in March, up from $60 in January. Energy prices are up 24% in 2026. At its April 29 meeting, the Federal Reserve explicitly cited the Middle East conflict as an inflation input — formally wiring a geopolitical event into the rate path.

That rate path is about to change hands. Warsh takes over May 15 with a stated agenda to narrow the dual mandate toward inflation-only, overhaul the 2020 average inflation targeting framework, and reduce reliance on unconventional tools. He inherits an economy where the primary inflation driver is a war that ended five weeks ago but hasn’t normalized.

April CPI lands Tuesday. If it comes in hot, Warsh inherits an actively deteriorating inflation picture in his first week. If it moderates, the thesis softens quickly. That single data point is the most important input of the week — and it lands before the summit, before the handoff, and before markets have time to process any of it.

Top Risk: RK-005 — Critical Infrastructure Cyber Attack

Score: 80 (Elevated) · High confidence · Held

Iranian IRGC-affiliated group CyberAv3ngers remains confirmed-active against US water, energy, and government operational technology systems — PLCs that control physical infrastructure. CISA Advisory AA26-097a (April 7) documented at least 75 compromised core automation devices and confirmed disruptions in March–April. CISA launched CI Fortify on May 5 in direct response. No new advisory has been issued in 31 days, which may reflect successful containment at current scale or an operational pause.

What hasn’t changed: the ceasefire doesn’t stand this risk down. Iranian cyber programs are persistent and predate the kinetic conflict. FINRA’s precautionary alert for the financial sector remains active — not a confirmed incident, but a leading indicator of where attention is focused.

The base scenario holds: active campaigns continue at current scale, CISA accelerates mandatory ICS/OT reporting requirements, and OT/ICS security spending compounds on a regulatory tailwind. FTNT and TENB are the most accessible public proxies; Claroty and Dragos are the specialist private names to watch for IPO or acquisition activity.

Bear trigger: A new CISA advisory confirming attacks on financial system infrastructure or bulk power grid.

Deep Dive: RK-002 — Federal Reserve Policy Path Uncertainty

Score: 36 (Watch) · Medium confidence · ↑ +12 this cycle

Two independent signals drove the escalation. First, March CPI printed 3.3% YoY — headline driven by a 21.2% monthly gasoline spike, the largest since 1967, directly traceable to the Iran War’s Strait disruption. Core CPI held at 2.6%, meaning the pressure is isolated but not yet systemic. Second, Warsh cleared the Senate Banking Committee 13-11 on April 29, the first fully partisan Fed chair confirmation in US history. Full Senate vote expected this week; handoff May 15.

Bull (p=0.20): April CPI moderates meaningfully; Warsh governs more cautiously than pre-confirmation statements suggested — historical norm for incoming chairs. Fed signals path toward cuts in H2. Rate-sensitive assets recover; dollar softens.

Base (p=0.55): CPI prints in the 2.8–3.2% range; Warsh confirms and makes measured opening statements; policy path adjusts cautiously with one cut in late 2026. Dollar remains firm; credit spreads stable but elevated.

Bear (p=0.25): CPI above 3.2%; Warsh’s first statements reaffirm mandate-narrowing agenda; higher-for-longer read dominates. Credit spreads widen; TLT under pressure; EEM outflows accelerate as dollar strengthens.

The Iran War is the upstream driver — if Strait traffic normalizes faster than expected, the primary CPI input moderates and the bear scenario loses its main fuel. That is also the fastest route to the bull scenario.

Bear trigger: April CPI above 3.2% combined with hawkish Warsh opening statements. Either alone is manageable; together they are the scenario.

The Others

RK-005 — Critical Infrastructure Cyber Attack (80, held): Iranian IRGC-affiliated attacks on US water, energy, and government OT/ICS systems continue at confirmed-active scale. No Tier 1 escalation as of May 8; FINRA alert remains precautionary. Base scenario intact.

RK-001 — US-China Semiconductor Export Controls (48, held): Trump-Xi summit May 14–15 is the near-term catalyst, but Iran is expected to crowd out semiconductor discussion. Score held pending summit outcome; rescore by May 16.

RK-003 — China–Taiwan Strait Tension (40, held): PLA Liaoning carrier and Type 055-led task group deployed in late April as Balikatan 2026 mirror responses — strategic signaling, not Taiwan-specific escalation. Diplomatic window ahead of summit suppressing near-term provocations.

RK-004 — AI Regulatory Crackdown (9, Monitor): EU Digital Omnibus provisional agreement May 7 deferred high-risk AI compliance to December 2027. Combined with US federal preemption EO, near-term regulatory pressure materially lower. Reclassified to Monitor.

RK-006 — Iran War Post-Ceasefire Fragility (45, new): Ceasefire holds but Strait at 5% capacity; Iranian government in post-Khamenei transition; proxy networks active. Base scenario: partial Strait disruption through H2, oil at $80–95. Cross-linked to RK-002 (inflation channel) and RK-005 (cyber campaign origin).

What Could Be Wrong

The Warsh risk may be overstated. Historical precedent is nearly universal — incoming Fed chairs govern more cautiously than pre-confirmation statements imply. FOMC consensus is hard to move unilaterally; Warsh will need to build it. If April CPI shows normalization and his opening statements are measured, the bear scenario for RK-002 deflates rapidly. The 13-11 partisan vote signals political friction, not necessarily policy radicalism.

What to Watch

April CPI — May 12, 8:30am ET (RK-002): Above 3.2% increases bear scenario probability. Below 2.8% supports normalization narrative and eases RK-006.

Warsh first statements — on or after May 15 (RK-002): Any language on mandate interpretation or framework overhaul is the next signal.

Trump-Xi summit communiqué — May 14–15 (RK-001, RK-003): Watch for semiconductor language (bull trigger for RK-001) and Taiwan stabilization language (bear suppressor for RK-003).

Post-summit PLA response — within 14 days (RK-003): A named exercise announcement within two weeks of the summit is the bear scenario trigger.

Strait of Hormuz vessel traffic (RK-006): Normalization toward 30%+ of pre-war levels is the primary disinflationary input for RK-002.

Sources Used This Issue

Government & Regulatory

CISA Advisory AA26-097a — Iranian ICS/OT attack campaign (RK-005)

FINRA Cybersecurity Alert, 2026 (RK-005)

BLS Consumer Price Index, March 2026 (RK-002)

Federal Reserve FOMC statement, April 29, 2026 (RK-002)

EU Council press release, May 7, 2026 — Digital Omnibus on AI (RK-004)

ROC Ministry of National Defense — PLA activity data, May 4, 2026 (RK-003)

Research Institutions

World Bank — Commodity Markets Outlook, April 28, 2026 (RK-006)

IMF — Middle East war economic impact, March 2026 (RK-006)

CFR — Warsh confirmation hearing analysis (RK-002)

Atlantic Council / Brookings — Trump-Xi summit preview (RK-001)

AEI — China-Taiwan Update, May 1, 2026 (RK-003)

News & Analysis

CNBC — Warsh confirmation; Iran focus at Trump-Xi summit (RK-001, RK-002)

The Diplomat — PLA Liaoning carrier assessment (RK-003)

Unit 42 / Palo Alto Networks — Iranian APT threat brief, April 17, 2026 (RK-005)

Legal & Compliance

IAPP / Hogan Lovells — EU AI Act Omnibus analysis (RK-004)

Research Disclaimer: This publication is for informational and scenario-analysis purposes only. Nothing here constitutes financial advice, investment recommendations, or a solicitation to buy or sell any security. All analysis reflects the operator’s interpretation of available information and may be incomplete, incorrect, or outdated. Confidence levels reflect analytical judgment, not probabilistic certainty. Always consult a licensed financial advisor before making investment decisions.

Gatherthink Signals publishes weekly under the GatherThink Substack. Archives and full risk register available to paid subscribers.